Insurance Sales Agents

Explore safer careers (4)

Lower estimated automation risk

Why it fits

Uses client goals, risk needs, household finances, regulated products, relationship management, and financial explanations.

Why it fits

Fits experienced agents using pipeline review, coaching, targets, prospecting strategy, negotiations, and sales metrics.

Why it fits

Transfers regulated financial sales, suitability discussions, client relationships, market updates, and compliance habits.

Why it fits

Uses client interviewing, household risk, debt and cash-flow discussions, education, action plans, and confidential records.

Occupation snapshot

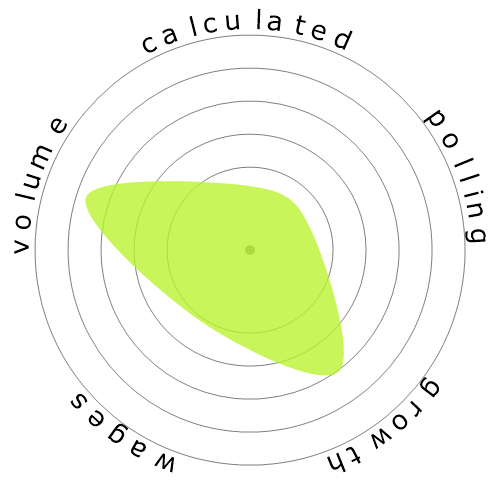

What does this snowflake show?

What's this?

We rate jobs using four factors. These are:

- Chance of being automated

- Job growth

- Wages

- Volume of available positions

These are some key things to think about when job hunting.

Risk & user votes

Calculated automation risk

Moderate Risk (41-60%): This occupation may be meaningfully affected by automation. Some parts of the role may be suitable for AI, software, or robotics, while others still rely on human skill, judgement, trust, or real-world context. People in this range may benefit from building skills that complement automation and reduce replacement risk.

More information on what this score is, and how it is calculated is available here.

Human strengths important in this job

These are human abilities and work contexts that are important in this occupation. They may help explain why parts of the role are harder to replace end-to-end, but they are not the only inputs into the automation score.

Persuasion

Quite importantWhy this matters

Working directly with the public

Quite importantWhy this matters

Thinking creatively

Quite importantWhy this matters

Social perceptiveness

Quite importantWhy this matters

Critical thinking

Quite importantWhy this matters

Show 3 more strengths

Developing objectives and strategies

Quite importantWhy this matters

Active learning

Quite importantWhy this matters

Education and training expertise

Quite importantWhy this matters

What users think

Based on 275 votes

Our visitors have voted they are unsure if this occupation will be automated. This assessment is further supported by the calculated automation risk level, which estimates 49% chance of automation.

What do you think the risk of automation is?

What is the likelihood that Insurance Sales Agents will be replaced by robots or artificial intelligence within the next 20 years?

Sentiment

Based on user votes over time

View sentiment trend

How opinions have changed over time

Pay & outlook

Wages

In 2024, the median annual wage for Insurance Sales Agents was $60,370 ($29 per hour).

The median annual wage for Insurance Sales Agents was 22.0% higher than the national median annual wage, which stood at $49,500.

View wage trend

Wages over time

Growth

The number of 'Insurance Sales Agents' job openings is expected to rise 3.7% by 2034

View employment trend

Total employment, and estimated job openings

Updated projections are due 09-2025.

Volume

As of 2024 there were 469,480 people employed as 'Insurance Sales Agents' within the United States.

This represents around 0.30% of the employed workforce across the country

Put another way, around 1 in 328 people are employed as 'Insurance Sales Agents'.

People also viewed

Job description

Sell life, property, casualty, health, automotive, or other types of insurance. May refer clients to independent brokers, work as an independent broker, or be employed by an insurance company.

O*NET-SOC code: 41-3021.00

What people are saying (25)

As for the insurance agent, AI can easily understand and sell a product. One could argue that using AI will increase the risk of E&O. That may be true, but 1) AI will improve and the E&O risk will greatly decrease and 2) The cost to use AI, and pay the salary of one or a team of specialists to maintain the AI will save so much on employee salaries (AI +3-5 people can easily replace 100+ agent departments) that the cost for E&O deductibles and possible E&O premium increase is outweighed. 100 agents making $60k/year = $6,000,000 saved.

An AI can do the same. Key in custom values and voila, a carefully crafted plan will be ready for you. And it may even analyse existing clients and suggest the most suitable plan for you. If you feel unsure about their decision and have more spare cash, you can raise the premium and decide to insure more.

Also, yes, you can buy insurance online, but I can't tell you how many times I had to go fix a problem or amend a policy because someone did it online and did not fully understand what they were doing.

Reply to comment