Insurance Underwriters

Explore safer careers (5)

Lower estimated automation risk

Why it fits

Fits underwriters using records review, inconsistencies, risk flags, interviews, evidence, and written case summaries.

Why it fits

Fits data-focused underwriters using risk metrics, reports, data quality, trend review, and business recommendations.

Why it fits

Applies rule interpretation, audit trails, policy standards, records, exceptions, and corrective documentation.

Why it fits

Uses financial applications, risk decisions, borrower facts, documentation, guidelines, and customer explanations.

Why it fits

Reuses insurance products, coverage limits, customer risk questions, applications, and policy explanations with sales shift.

Occupation snapshot

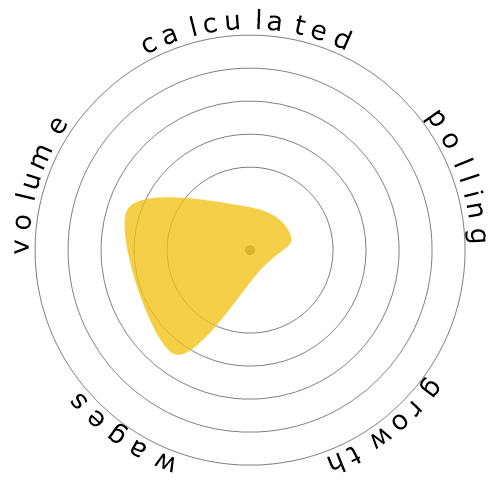

What does this snowflake show?

What's this?

We rate jobs using four factors. These are:

- Chance of being automated

- Job growth

- Wages

- Volume of available positions

These are some key things to think about when job hunting.

Risk & user votes

Calculated automation risk

Moderate Risk (41-60%): This occupation may be meaningfully affected by automation. Some parts of the role may be suitable for AI, software, or robotics, while others still rely on human skill, judgement, trust, or real-world context. People in this range may benefit from building skills that complement automation and reduce replacement risk.

More information on what this score is, and how it is calculated is available here.

Human strengths important in this job

These are human abilities and work contexts that are important in this occupation. They may help explain why parts of the role are harder to replace end-to-end, but they are not the only inputs into the automation score.

Decision-making and problem solving

Very importantWhy this matters

Communicating with people outside the organization

Very importantWhy this matters

Social perceptiveness

Quite importantWhy this matters

Active learning

Quite importantWhy this matters

What users think

Based on 197 votes

Our visitors have voted that it's probable this occupation will be automated. This assessment is further supported by the calculated automation risk level, which estimates 58% chance of automation.

What do you think the risk of automation is?

What is the likelihood that Insurance Underwriters will be replaced by robots or artificial intelligence within the next 20 years?

Sentiment

Based on user votes over time

View sentiment trend

How opinions have changed over time

Pay & outlook

Wages

In 2024, the median annual wage for Insurance Underwriters was $79,880 ($38 per hour).

The median annual wage for Insurance Underwriters was 61.4% higher than the national median annual wage, which stood at $49,500.

View wage trend

Wages over time

Growth

The number of 'Insurance Underwriters' job openings is expected to decline 2.6% by 2034

View employment trend

Total employment, and estimated job openings

Updated projections are due 09-2025.

Volume

As of 2024 there were 107,820 people employed as 'Insurance Underwriters' within the United States.

This represents around 0.07% of the employed workforce across the country

Put another way, around 1 in 1 thousand people are employed as 'Insurance Underwriters'.

People also viewed

Job description

Review individual applications for insurance to evaluate degree of risk involved and determine acceptance of applications.

O*NET-SOC code: 13-2053.00

What people are saying (8)

I am considering entering insurance underwriting because claims were very bad, I must say.

Would you say that computer automation is taking over all areas of underwriting (commercial underwriting, property & casualty underwriting, etc.)? I do hear that it is taking personal insurance by storm.

Also, I am REALLY trying hard to find similar jobs to underwriting/insurance in case underwriting doesn't work out.

I'm looking at cost estimating (outside of construction), property assessment, and budget analysis. According to the Bureau of Labor Statistics, you don't necessarily need a business or finance degree to go into these fields (I took several traditional/core business classes in school, and I also majored in a field much like "business psychology" - organizational development, which was in the business school).

Do you have any alternatives that you plan to explore in case you have to leave underwriting? Do you think any of the ones that I mentioned are feasible alternatives?

Thank you,

Carl Daniel

Do you mean to say that this definition removes the need for an underwriter? - "Review individual applications for insurance to evaluate the degree of risk involved and determine the acceptance of applications."

Oh, sorry, I just realized that you mentioned that this definition only applies to line underwriting, and that automation will decrease the need for line underwriters.

Thank you for clarifying that there are two types of underwriting - I wasn't aware of that. Underwriting is the only field in insurance that interests me, but I'm not into sales. I've been working in claims (and subrogation) for years, but it's not my cup of tea.

Since I don't have the educational background to be an actuary, underwriting is pretty much the only option left for me.

I've never heard of staff underwriting before - unfortunately, working in claims didn't teach me much about underwriting.

It seems like staff underwriting is the future of employment in underwriting.

You mentioned that commercial insurance/underwriting is hard to predict due to the constantly evolving and complex nature of insurance.

I'm considering getting my Associates in Commercial Underwriting while I search for a job in underwriting.

What do you think about the future of employment in commercial underwriting? Do you think there's any hope for cautious optimism, especially for staff underwriters in commercial underwriting?

Thank you,

Carl Daniel

Reply to comment